Published - February 17, 2023 @ 3:06 PM (CET)

A fortnight ago, Spotify (NYSE:SPOT) announced its quarterly results for the fourth quarter of 2022. The figures missed analyst expectations and caused an upward move in the stock. Nevertheless, Spotify in general is still in turbulent waters and just recently announced that it is laying off 6% of its employees worldwide. Is danger lurking around the corner or does the future look bright?

Spotify Technology SA is a Luxembourg-based company, but of Swedish origin, dedicated to offering digital music, podcast and video streaming services. The company allows its users to discover the latest song releases, both singles and albums, as well as playlist created by other fans or music connoisseurs and gives access to millions of songs, podcasts and more. In doing so, it differentiates between Spotify Free and Spotify Premium.

The Spotify Free version available for free to all users gives access to the entire music offering, but limits the features to the use of shuffle play. Spotify Premium, on the other hand, gives users access to a range of features, including shuffle play, as well as disabling ads, unlimited song skipping and offline listening. Spotify is available in more than 20 countries.

Recent quarterly results (4Q 2022)

As cited earlier, despite failing to turn a profit, Spotify performed better than the market had expected. The biggest reason for joy was that the company was able to post a 20% year-on-year growth in its number of active monthly users to 489 million. This is a net increase of a whopping 33 million users compared to the third quarter. The number of paying users increased 14% year-on-year to a total of 205 million by the end of 2022. At the end of September, the company still announced that it assumed a user base of 479 million, including 202 million paying subscribers.

Last quarter's revenue of €3.16 billion was below its own expectations of €3.20 billion, but in line with analyst expectations. An increase of 14% for revenue derived from offering advertising space on the platform, which made up 14% of total revenue, was mainly driven by growth in the podcasts segment.

The operating result came to a loss of 231 million euros, where it recorded a loss of only 7 million euros last year. The biggest factor in this appeared to be a sharp 44% year-on-year increase in operating expenses, mainly due to an oversized workforce (32% vs 2021) and higher advertising expenses. Earnings per share came in at a loss of €1.40, with negative free cash flow of €73 million.

The company also revealed that it will say goodbye to about 600 employees, or 6% of its global workforce. This is to cope with the tougher economic situation causing consumers and advertisers worldwide to scale back their spending.

Reason for concern?

The fact that with such user numbers, Spotify, as the biggest player in the audio streaming market, still cannot make a profit raises questions for many an investor.

A key factor in the quest for profitability is the problematic business model the company employs whereby it pays out about 75 cents per dollar earned, 75% of revenue, as royalties to record labels. In this way, a limited portion of the incoming cash flow always remains for the business operation itself. Spotify itself points to a change in its business model where it wants to focus more on the podcast segment, where this problem is no longer an issue as all revenue generated will be for the company. However, the loss in the last year was just partly caused by this. To make the pivot towards the podcast segment, a lot of money was spent on signing exclusive contracts with current podcast luminaries like Joe Rogan and Dax Shepard.

Another pain point Spotify is facing is that it is having a lot of trouble pricing its offerings. Whereas the biggest players within certain markets normally have the competitive advantage and can push through their pricing, Spotify seems unwilling or, worse, unable to raise prices here. In the world of paid music streaming, the company mainly has to contend with competitors like Alphabet with Youtube premium and Apple Music. Despite both not being direct competitors within this market segment, they are responsible for snatching away customers who might otherwise have found their way to Spotify Premium. Both competing services also recently raised the prices of their services. The difference with Spotify is that these two tech giants can indeed afford to make a loss on their segment within music streaming because it is part of a much broader offering, with the bulk of their revenue coming from elsewhere.

Current valuation and outlook

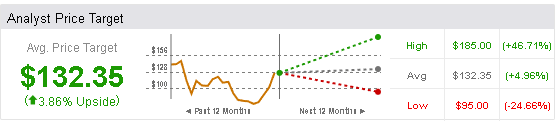

The stock is currently trading around $127 and has a moderate buy recommendation among 20 analysts over the past 3 months, with an average price target of $132.35, offering upside potential of about 4%.

The average analyst expectation reflects the market's caution towards recent commitment to cost-cutting to improve profit margins over time. It will take some time to see if this trend can be sustained and provide the hoped-for results. One positive sign in any case is that Spotify seems to be managing to improve its ad revenues quarter-on-quarter.

Spotify's management expects to round the mark of 500 million monthly active users in the first quarter of 2023, an increase of 11 million new users. It also expects a loss of 194 million euros on quarterly revenue of 3.1 billion euros.

So it remains to be seen whether the audio streaming giant can continue its revenue from ads and its switch to becoming YouTube for podcasts in the near future.

.jpg)